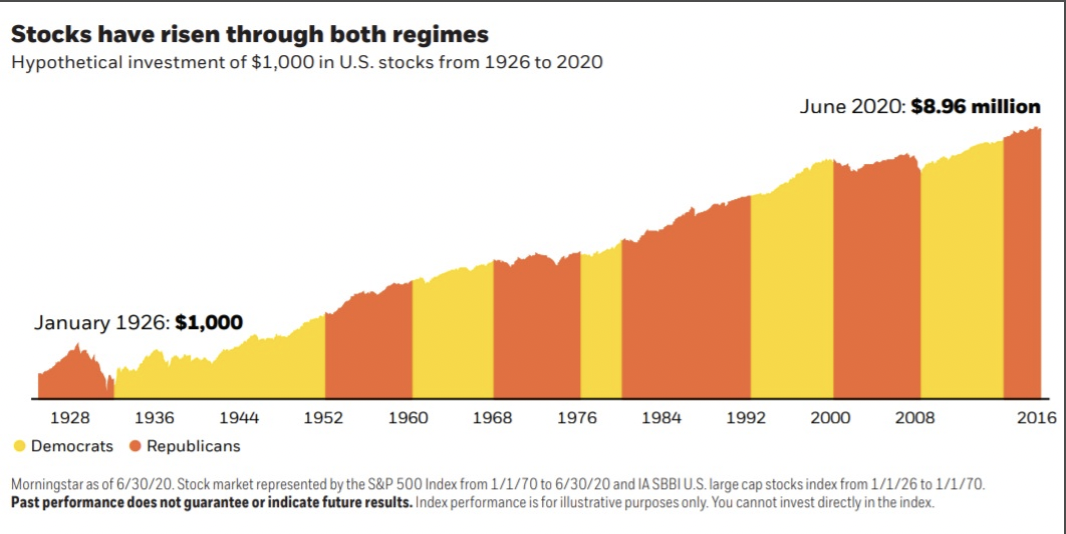

Just as economies around the world are regaining momentum after the pandemic shut them down, investors are now facing the uncertainty of a U.S. presidential election in an increasingly polarized nation. With elections approaching, many investors tend to consider which political party might be better for the market. But history tells us that over the long run, the market doesn’t care who is in control of the White House. Since 1926, markets have continued to rise regardless of which party holds office. We are covering some key considerations below as they pertain to the election and how we are moderately shifting portfolios and our investment outlook for this quarter.

Key Takeaways

Taking some risk off the table amidst election uncertainty

As we enter the home stretch of election season in the United States, Democratic nominee Joe Biden looks to have an edge in the race. We see three plausible scenarios to plan for: 1) a Democratic sweep of the White House and Congress (with Democrats winning control of the Senate); 2) a Biden win with a divided Congress; and 3) a status quo Trump win. The pandemic has helped create historically challenging circumstances for the election, including a leap in mail in voting that adds complexity and increases the probability of legal challenges. A contested election could delay a definitive outcome for weeks or months. With this increasing uncertainty potentially driving up market volatility, we are trimming risk in the portfolios by cutting our equity overweight and trimming some cyclical stock exposure.

Changing the play on cyclicals to add protection

Our thesis from earlier in the year called for rising stock prices supported by improving Covid-19 abatement efforts, easing of economic lockdowns, and an ultra-accommodative Federal Reserve. Our strategic tilts to technology and large-cap stocks have led the way so far in the early recovery – but some of our more tactical bets on cyclically-oriented stocks have been slower to payoff. These more volatile, cyclical names are used to fund a modest rotation into more resilient, higher-quality exposures. Nonetheless, despite the election risks, we maintain conviction in our view of a broader economic recovery, so continue to be slightly overweight stocks and hold barbell positions in both large-cap/growth while increasing the duration of fixed income.

Seeing opportunities in EM underdogs

China has been leading the economic rebound in global output, with other emerging economies across Asia on similar paths to robust recoveries. The potential for a resurgence in trade tensions pose risks to sentiment, but if improving economic data trends continue, then the case for EM equities becomes stronger. Conversely, we have seen a lukewarm recovery and weaker revisions to earnings estimates in Europe, especially vis-à-vis the US and EM. To potentially capitalize on this divergence, we are decreasing exposure to DM stocks and adding to EM stocks.

Trade Details:

- We are trimming equities by 1%. While we don’t see a Biden or Trump presidency with a divided Congress as a decidedly risk-off event, we believe it’s prudent to cut risk in case potentially more adverse outcomes materialize.

- The portfolios increase exposure to higher-quality large cap stocks and reduce exposure to more volatile small cap stocks, bolstering overall resilience to potential election and Covid-19 related shocks.

- We are eliminating exposure to financial services stocks. The Fed’s ultra-dovish shifts in forward guidance and average inflation targeting, coupled with recent regulatory actions and investigations have materially impacted our prior conviction in this sector.

- The active short duration position is eliminated to help fund a position in mortgage-backed securities, with the goal of further insulating portfolios from a risk-off event.