In a historically challenging 2022 year to date, we continue to see market volatility as the Fed grapples with its response to the global problem of inflation, the Russia-Ukraine conflict continues to impact pricing, and China’s renewed lockdowns cause fresh supply chain issues.

Even with these concerns, we see strong U.S. Labor market employment data, signs that inflation could reach its peak this year, and meaningful progress in the Fed’s objective to tighten financial conditions and cool the economy.

If you haven’t seen it yet, we encourage you to watch our CEO Marty Miller’s video, “What’s causing volatility today?” published on May 5th. Click here to watch Marty’s video on market volatility.

Key Takeaways

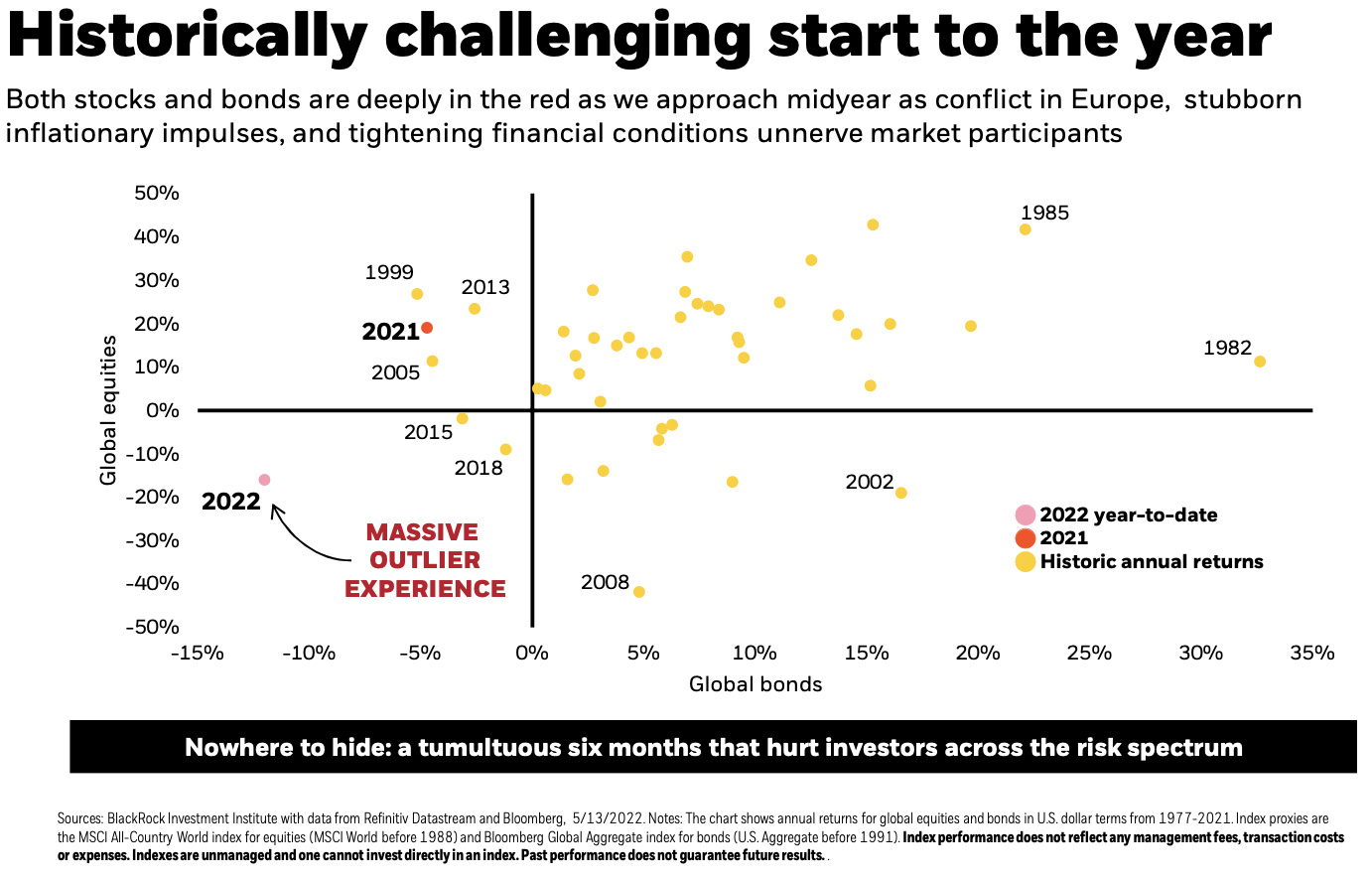

Historically challenging start to the year

With global stocks down 16% and global bonds down 12% as of May 13th, we’ve seen unprecedented losses in both stocks and bonds. Even in a historical context, as you can see from the graph above, 2022 is an outlier when we look at returns since 1977.

That being said, while painful, we believe it is still a normal experience for the market to go sideways at the beginning of a rate hike cycle.

In our view, the environment reflects the challenge of unusually high inflation coupled with a slightly higher recession risk introduced by a more hawkish Fed.

- Elevated global inflation is a problem well-advanced, in the wake of the COVID-19 crisis and recovery boosted by stimulus packages and accommodative monetary policy.

- The market and fed are responding to that problem, clearly now in a rate-hike cycle and expectations of additional hikes in the next couple meetings.

- The Russian-Ukraine conflict also impacts global prices and contributes to tightening an already stressed supply chain.

Energy and commodities deliver strong active returns

Despite the challenges outlined above, we’ve seen energy and commodities as strong contributors to our overall portfolio performance.

We are anticipating commodities to be a highly volatile sector moving into Q3, and we will be locking-in profit gains in our tactical reallocations.

Diversification and active tilts have provided portfolio resiliency

Active tilts into both international and U.S. value stocks, as well as exposure to TIPs, have contributed positively to performance and helped provide portfolio resiliency.

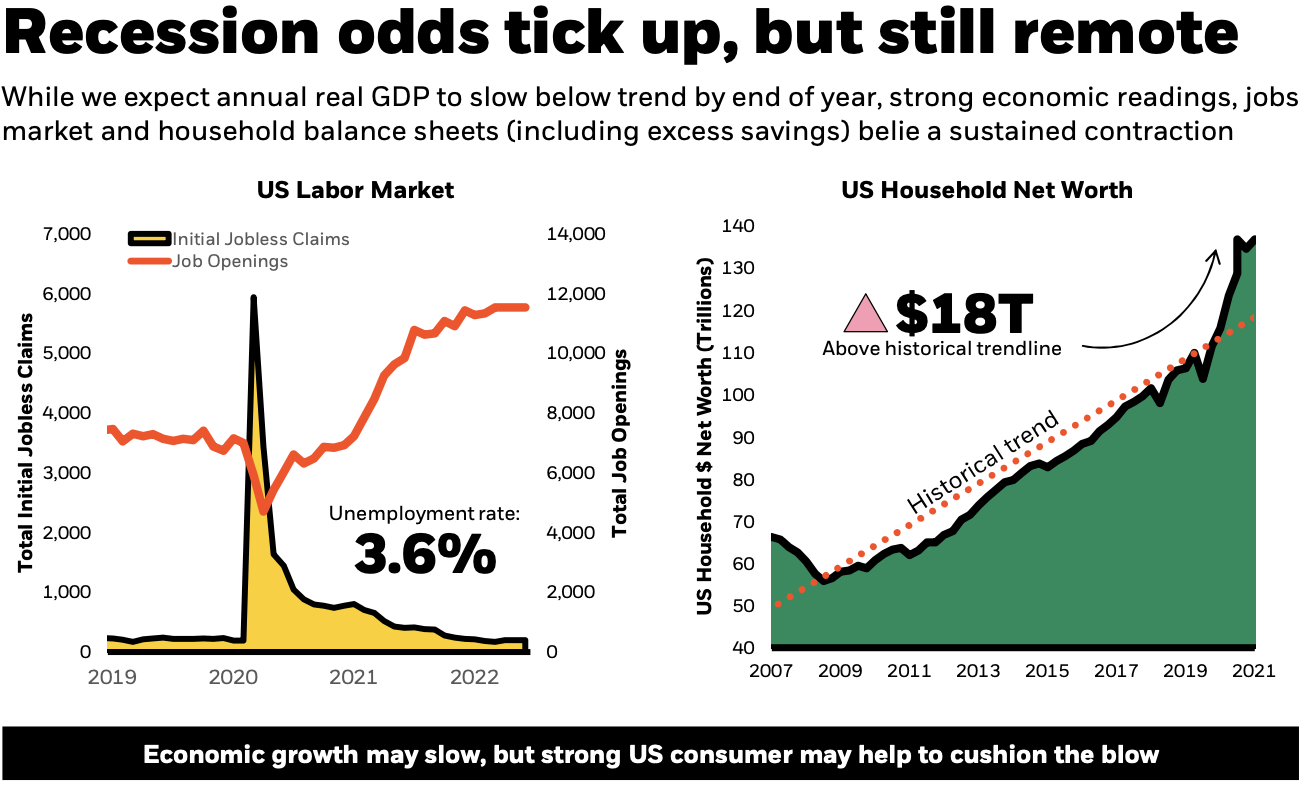

Recession odds tick up, but still remote

In a stark reversal from the trend seen in 2021, when the U.S. economy grew by 5.7%, the U.S. economy unexpectedly shrank by 1.4% in the first quarter of 2022.

While we expect annual real GDP growth rate to slow with planned rate increases, strong US economic data leads us to believe that growth slowdown will bring us back to a more neutral economic state. We do not anticipate a state of sustained contraction or recession.

As seen in the graph above, the U.S. Labor market remains strong and tight, with the unemployment rate sitting at 3.6% and the number of unemployed persons around 5.9 million - both these numbers are close to pre-COVID levels in February 2020.

U.S. consumers, who drive ⅔ of the overall economy, are benefitting from elevated U.S. household net worth currently $18T above the historical trend line.

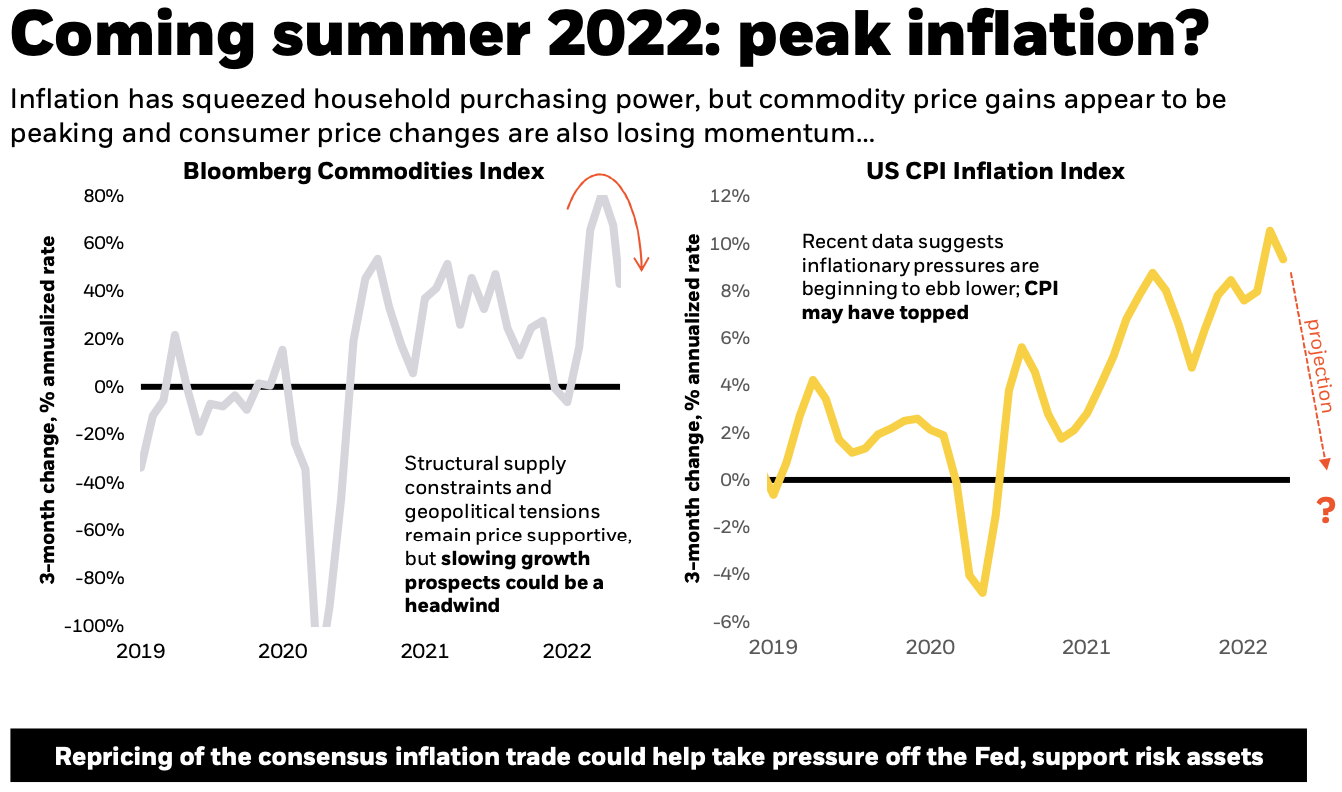

Peak inflation coming soon?

Inflation appears to be peaking; however, the risk of policy error has risen as the Fed struggles to keep inflation expectations anchored until supply catches demand.

While high wage growth, shelter costs, and low unemployment are likely to keep inflation above the Fed’s 2% target in the longer-term, near-term price pressures can be attributed to:

- supply and demand imbalances caused by the pandemic-induced shift in consumer spending from services to goods

- the supply shock in energy and commodities markets ignored by the Russia/Ukraine conflict

- fresh supply chain disruptions as China renews Covid-19 lockdowns

Our interpretation is that unusually low supply is still pushing prices higher, rather than unusually high demand pulling prices upward. Supply-driven inflation is still the culprit.

The Fed is faced with a difficult decision: either choke off growth via higher interest rates or accept persistent above trend inflation. We believe the Fed will choose to live with higher inflation, but the risk of a recession is clearly rising.

Fortunately, there are signs inflation could be peaking:

- Demand is stabilizing as goods price growth slows while service prices rise quickly

- Wage growth rates are slowing as labor force participation rate increases

- Supply chain problems are easing

- Commodity price pressures are stabilizing

Here are the main risks to inflation hitting its peak:

- The central bank could perceive excessively high demand as the economy overheating and raise rates to a level that will deliberately slow growth, or

- Even without tangible action, the market could become convinced that the central bank will take this action.

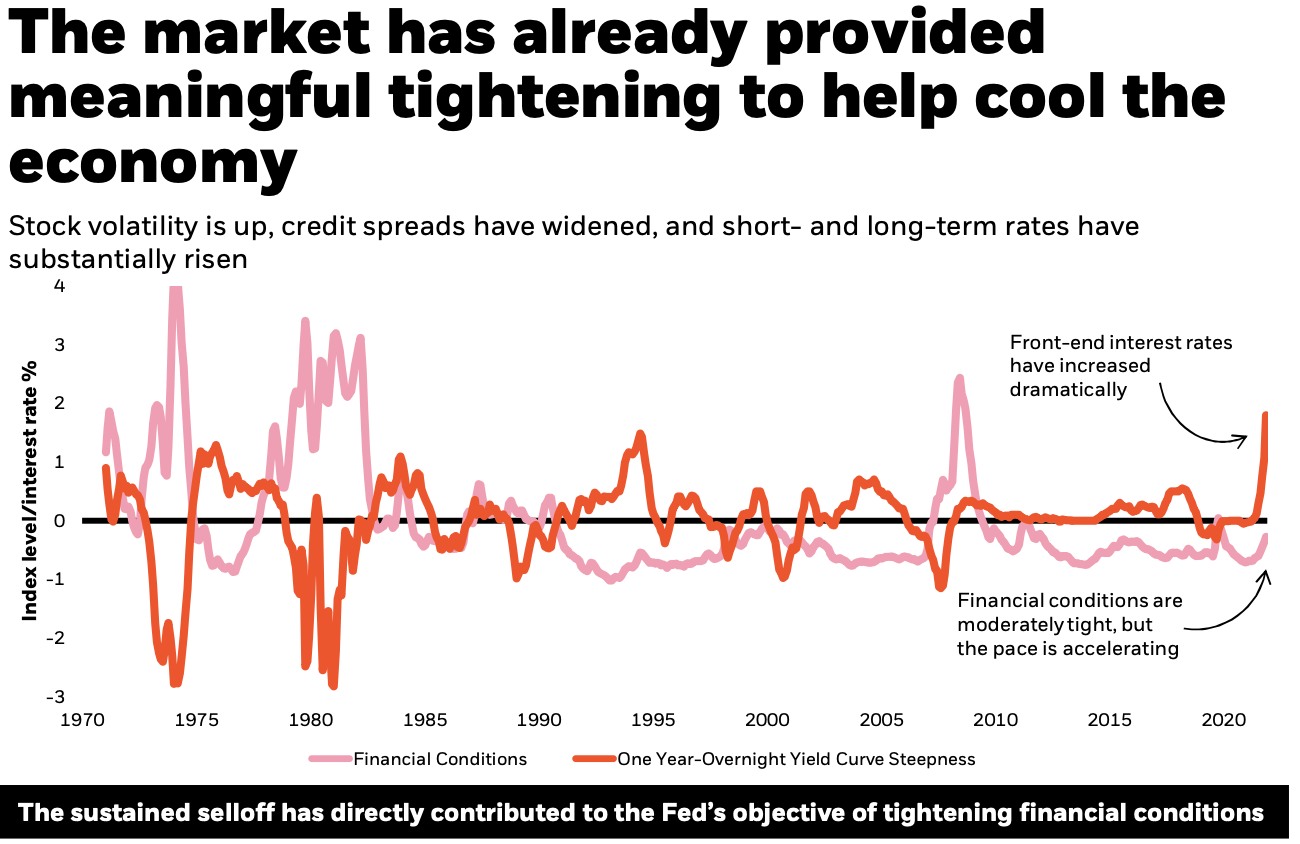

Market has already provided meaningful tightening to help cool the economy

As long as inflation remains well above the Fed’s 2-3% comfort level, we expect to see continued moves to normalize rates, reduce excess demand, and bring the labor market into better balance.

That being said, the sharp and sustained selloff across markets has directly contributed to the Fed’s objective of tightening financial conditions. From this graph, we see the recent dramatic increase in front-end rates correlated with an acceleration in tightening financial conditions.

Year to date, investors have seen stock volatility elevated, credit spreads widening, and both short and long term rates rising substantially: all contributing to the desired effect from the Fed to cool the economy and combat high inflation levels.

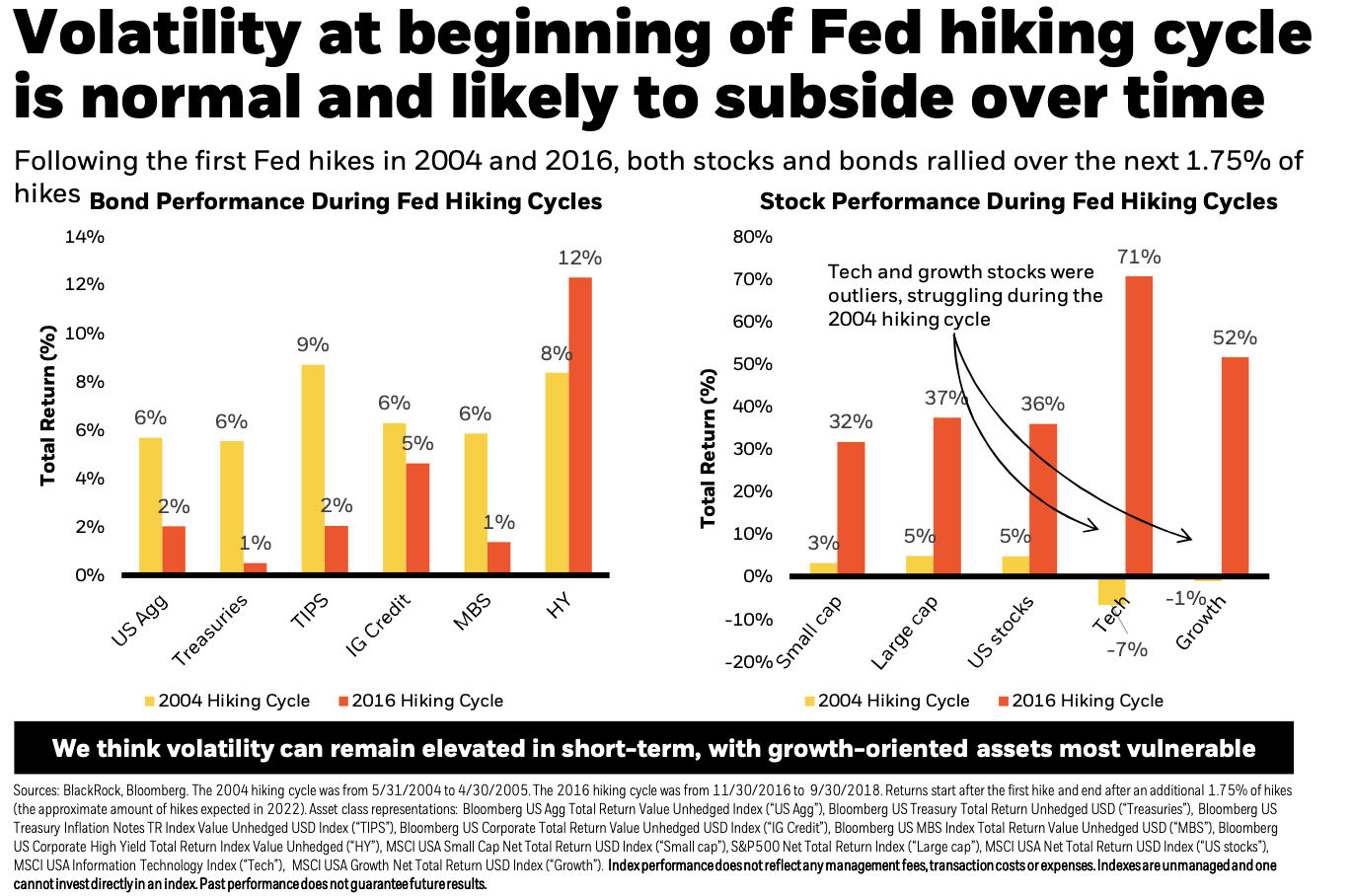

Volatility at beginning of Fed hiking cycle normal and likely to subside over time

We do expect near-term volatility to remain elevated; however, the market has rapidly priced in a series of new policy data points, adding some clarity to the shape of the Fed’s hiking cycle.

- 12 months ago, the market was pricing in 0 rate hikes in 2022 and 2023.

- 6 months ago, the market was pricing 1 hike in 2022 and 3 in 2023.

- Today, the market is pricing in 7 hikes this year alone.

Looking back at the last two Fed hiking cycles (in the graphs above), we can see that after the first hike, both stocks and bonds rallied. Once the market prices in the new monetary policy, all of the uncertainty around rates is alleviated.

With all the other sources of uncertainty, we are hesitant to extrapolate this trend forward to today; however, it is plausible that the majority of policy induced asset repricing is behind us.

- Stocks have been selling off based on recession fears, but bond yields are rising with the yield curve steepening, suggesting a stronger economy and no recession.

- We would see more reason to anticipate trends from 2004 and 2016 repeating themselves here if: the Fed’s tightening starts to rein in inflation expectations further and supply/demand dynamics cool headline inflation.

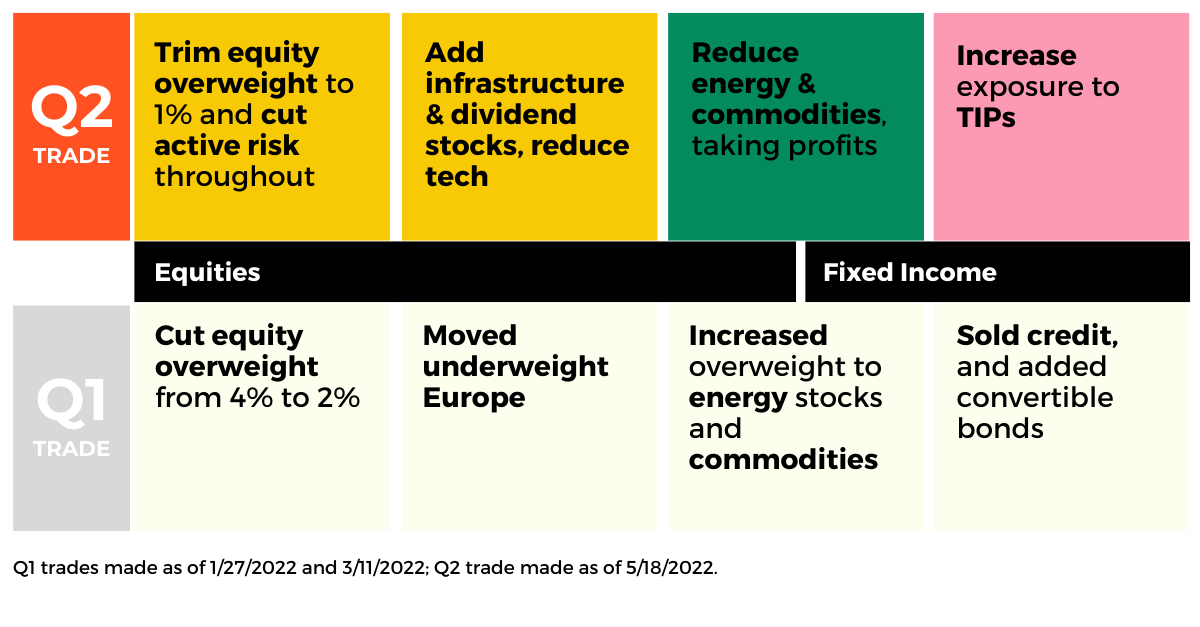

Trade Details*

*Tactical changes are dependent upon your investment strategy and risk tolerance.

Our trades reflect a continued emphasis on adding portfolio resilience and reducing volatility throughout 2022.

- Trim equity overweight, but maintain a preference for stocks over bonds, with a focus on adding portfolio resilience

- Reduce overall sensitivity to growth and volatility, cutting net exposure to technology and credit

- Lock-in profits on commodities and energy stocks after handsome rallies

- Introduce exposure to US infrastructure and dividend-focused stocks, which have historically delivered attractive relative returns during periods of tightened financial conditions

- Increase exposure to inflation-protected US Treasuries (“TIPS”), potentially providing less downside if nominal rates rise further and tactically hedging against further upside surprises in inflation expectations

- Remain underweight emerging market stocks, and further aim to de-risk by rotating into names that have historically exhibited lower volatility characteristics